Roofing Project Financing Questionnaire for Homeowners

Before you start, don’t forget to download our free Roofing Sales Questionnaire for Homeowners. 80% of your sales results will come from knowing what questions to ask your prospect. The more relevant information you have on your prospect, the more customized your solutions will be, and you will be more likely to have your prospect buy from you. This is why you must download and use this roofing sales questionnaire.

For many homeowners, replacing a roof is a high-ticket, unplanned expense that can feel like a financial earthquake. How many deals have you lost because a prospect couldn’t afford the upfront cost? Homeowners rarely budget for a new roof, and when the need arises, cost becomes a major obstacle.

But for roofing contractors, this challenge presents a powerful opportunity. Your ability to offer or guide prospects toward viable financing solutions isn’t just a convenience; it’s the key to closing more deals and building a thriving business.

This isn’t just about offering loans; it’s about removing the biggest barrier to a homeowner saying ‘yes,’ transforming a daunting necessity into an achievable investment for their home.

Discover how we help with Roofing Lead Generation.

This comprehensive guide explores 17 financing options, empowering you to become a trusted advisor and a solution-oriented partner for your clients.

Are you positioned as a contractor who solves problems or installs roofs?

By mastering these strategies, you can transform cost objections into opportunities, allowing homeowners to protect their most valuable asset confidently.

Table of Contents:

- 1. Preferred Lender Partnerships

- 2. Home Equity Loans

- 3. HELOC (Home Equity Line of Credit)

- 4. Personal Loans

- 5. Credit Cards

- 6. Government-Sponsored Programs or Loans

- 7. Insurance Claim Assistance

- 8. Crowdsourcing

- 9. Family and Friends

- 10. 401(k) or Investment Portfolio

- 11. Savings: A Direct and Practical Approach

- 12. CDFI (Community Development Financial Institutions)

- 13. SBA (Small Business Administration) General and Disaster Loans

- 14. FHA 203(k) Loans

- 15. Life Insurance Policy Loan

- 16. PACE (Property Assessed Clean Energy) Programs

- 17. Manufacturer Financing Programs

- Closing the Deal

- The Path to a Thriving Roofing Business

- Our goal is to help organizations reach their growth goals

1. Preferred Lender Partnerships: Building a Network of Financial Allies

To effectively offer financing options, it’s crucial to form strategic alliances with 3 to 5 local or regional finance companies specializing in home improvement lending. This network should encompass lenders offering a spectrum of loan products designed to cater to diverse borrower profiles and needs. Do you currently partner with lenders who cater to different credit profiles and homeowner needs?

Explore Your Loan Options for Home Improvement

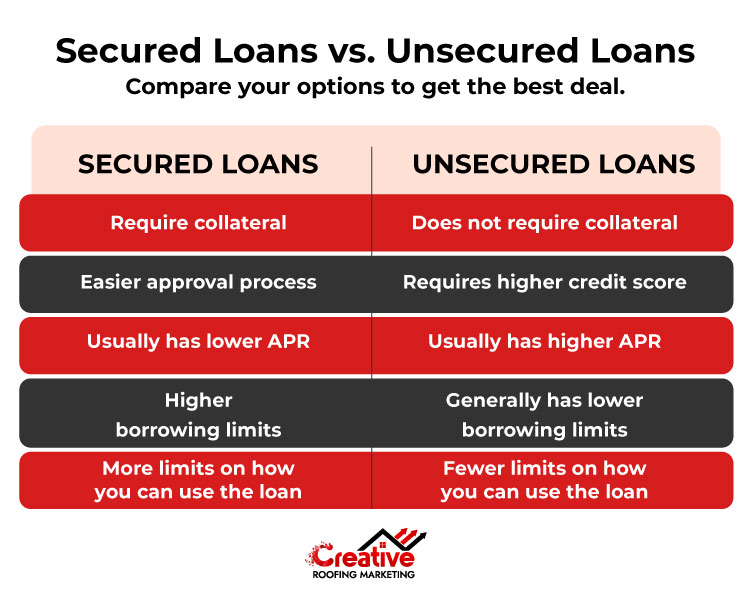

-No collateral required

-Faster approval process

-Typically higher interest rates

-Backed by collateral (e.g., home equity)

-Lower interest rates

-Stricter qualification requirements

-Tailored for renovation projects

-May offer better terms through specialized lenders

-Often easier to use for specific upgrades or repairs

Key Lender Criteria: When selecting lending partners, prioritize:

- Competitive Interest Rates: Negotiating preferred rates for your clients is essential.

- Flexible Loan Terms: Offer a range of repayment periods, such as 6 months to 10 years, to accommodate various budget constraints.

- Streamlined Loan Processes: Choose lenders known for quick approvals, minimal paperwork, and efficient funding to avoid project delays. A strong [Roofing Web Design] can also help streamline information flow.

- Strong Communication & Customer Service: Ensure your partners provide excellent communication throughout the loan process. Our commitment to [Completely Satisfied Customers] reflects this value.

Here are the Top 10 Questions for Roofers to Ask Finance Lending Partners

How To Present A Lender To A Roofing Prospect: When presenting lender options to homeowners, use language such as:

- “To make this project more affordable, we’ve partnered with several reputable lenders, including [Lender A], [Lender B], and [Lender C],”.

- “Interest rates start as low as [X%], and you can choose repayment terms that fit your monthly budget,”.

- “We can help you with the application process to ensure a smooth and hassle-free experience”. [Contact Us] for assistance.

How confident are you when discussing financing options with hesitant homeowners?

Action Step for Contractors: Research 3-5 local lenders, schedule meetings, and negotiate favorable terms for your clients. Ensure their application process is quick and hassle-free.

“By partnering with financing… contractors can stand out from competitors and win more jobs without extra charge or paperwork.”

– Steve Weyl of Able Roofing

2. Home Equity Loans: Leveraging Ownership for Affordability

For homeowners who have built substantial equity in their property, a home equity loan offers a lump sum of cash secured by that equity. The amount a homeowner can borrow is typically based on the difference between their home’s current market value and the outstanding mortgage balance.

- Ideal for Larger Projects: Home equity loans are often well-suited for larger roofing projects, such as full roof replacements, as they allow access to significant funds.

- Important Considerations:

- The loan is secured by their home, and failure to repay could lead to foreclosure.

- Lenders usually require a home appraisal to determine the property’s value.

- Home equity loans may involve closing costs, which should be factored into the overall financing decision.

How to Present A Home Equity Loan Option to Finance A Roofing Prospect: When presenting home equity loans to clients, you might say:

- “If you’ve owned your home for a while and have built up equity, a home equity loan is a powerful tool to finance a new roof,”.

- “The loan amount is based on your home’s value, and interest rates are often competitive,”.

- “We can help you determine if this option is right for you by providing a detailed project estimate for your lender”.

“Always remember to integrate financing as part of your sales proposal… customers often spend more when financing is offered.”

– IKO ROOFPRO

3. HELOC (Home Equity Line of Credit): Flexibility and Ongoing Access

A Home Equity Line of Credit (HELOC) functions as a revolving line of credit, much like a credit card, but it is secured by the homeowner’s equity in their home.

- Two Phases: This type of credit typically has two phases:

- A “draw period,” often lasting around 10 years, during which the homeowner can access funds as needed.

- A subsequent “repayment period,” commonly extending for 20 years, during which the outstanding balance must be paid back.

- Significant Flexibility: HELOCs offer significant flexibility, allowing homeowners to borrow funds in stages as their project progresses. This makes them particularly suitable for home improvement projects, such as roofing renovations that might involve phased payments or the need to address unexpected repairs.

- Variable Interest Rates: HELOC interest rates are frequently variable, meaning they can fluctuate based on market conditions over time. While some HELOCs may offer attractive low introductory rates, it is crucial to understand how these rates will adjust after the promotional period ends.

“They saw a 45% increase in project bookings and a 30% reduction in lost leads… a 78% boost in revenue within six months.”

How to Offer A HELOC Option to Finance A Roofing Project: When presenting HELOCs, emphasize their benefits and features:

- “A HELOC provides a flexible line of credit you can access as needed for your roofing project”.

- “It’s a good option if you’re planning other home improvements or want to have funds available for any unforeseen repairs”.

4. Personal Loans: Fast Access to Funds, Unsecured

Personal loans are unsecured. That means they’re not secured by the customer’s home as collateral.

- Lower Risk for Homeowners: This can be a big plus for homeowners because it makes it less risky for them, even if the interest rate might be a touch higher than, say, a home equity loan.

- Faster Approval: A huge advantage for us, and for the customer, is the faster approval process. When a roof is leaking, you need a fix fast, and personal loans can get that cash quicker than other options.

- Fixed Interest Rates: Most personal loans come with fixed interest rates. That’s great for the homeowner because their monthly payments will be predictable throughout the loan term.

- Credit Score Impact: The interest rate offered will depend heavily on their credit score. So, if they’ve got good credit, they’re likely to get more favorable terms.

If a prospect needs to finance roof repairs quickly and prefers not to use their home as collateral, a personal loan is absolutely a viable option. We can connect them with lenders who offer competitive personal loan rates specifically for home improvements. Just make sure they understand that their creditworthiness is going to be a key factor in what kind of rate they get.

“Client satisfaction increased by 95%, 88% positive reviews, and local market share rose 25%.” – Virginia roofing contractors

5. Credit Cards: Strategic Use for Short-Term Financing

For some homeowners, especially those with really good credit, a 0% introductory APR credit card can be a neat trick. It gives them a window of interest-free financing for their roof repairs. Plus, some of these cards even have rewards programs, meaning a little cash back or points, which is a nice bonus.

Crucial Considerations:

- Pay Off Before APR Expires: Homeowners need to be super careful and have the discipline to pay off the entire balance before that 0% APR period runs out. If they don’t, they’re going to get hit with some seriously high interest rates.

- Sufficient Credit Limit: They also need to make sure the credit limit is high enough to actually cover the whole roofing cost.

- Credit Utilization Ratio: Putting a big chunk of money on a credit card can temporarily bump up their credit utilization ratio, which might slightly ding their credit score for a bit.

So, if a homeowner is confident they can pay off the debt quickly, a new credit card with a 0% introductory APR can be a good short-term solution. It buys them some time to manage their finances without immediate interest charges.

It’s important to stress to the prospect that they have to have a solid repayment plan in place to avoid getting stuck with those high-interest charges down the road.

6. Government-Sponsored Programs or Loans: Seeking Public Assistance

There’s a good chance some of your clients might qualify for financial help with their roof repairs through various local programs. Many cities and counties offer things like grants, low-interest loans, or even deferred payment options specifically for home repairs, and that includes roofing.

- Eligibility: Usually, who’s eligible comes down to stuff like income, age, disability, or if they’re a veteran.

- Federal Resources: And it’s not just local; there are also federal resources through agencies like HUD or the USDA that might offer assistance.

- Energy Efficiency Incentives: On top of that, we should always talk about energy efficiency incentives. The federal government often provides tax credits if a client installs certain energy-efficient roofing materials. Plus, we need to check if local utility companies or even the government in their area offer rebates for those energy-saving roofing upgrades. That’s money back in their pocket!

How often do you check if your clients qualify for local grants, rebates, or tax credits?

Depending on their unique situation, a client might qualify for financial assistance through these local or federal programs. We can help them figure out what’s available and if they’re eligible.

And hey, pushing for an energy-efficient roof could snag them some valuable tax credits or rebates, which is a win-win for everyone.

7. Insurance Claim Assistance: Your Expertise as a Guide

First off, you’re telling them you can jump in and help them figure out if their homeowner’s insurance policy actually covers their roof damage. You want them to know that most policies usually kick in for stuff like windstorms, hailstorms, fire, vandalism, or even falling trees.

That’s the basic rundown, and they must hear it from you.

- Your Expertise: Next, you’re really emphasizing your expertise. You’re not just a roofer; you specialize in managing insurance claims. This means you’ll be the one meticulously documenting everything with photos and videos. You’ll put together a detailed and accurate estimate for the repairs or replacement.

- Direct Communication: And then, crucially, you’ll communicate and negotiate directly with the insurance adjuster on their behalf. To top it off, you’ll handle all the necessary paperwork, making the whole process as smooth as possible for them. It’s about taking the burden off their shoulders.

How To Present The Insurance Claim Assistance Option To Finance A Roof:

- We believe in transparency and setting realistic expectations. We’ll be honest about the limitations of your insurance coverage and clearly communicate what your insurance is likely to cover versus what you’ll be responsible for, such as your deductible.

- We’ll conduct a comprehensive inspection of your roof to determine if your insurance policy likely covers the damage.

- We have extensive experience working with insurance companies and can handle the entire claims process for you, minimizing your stress. Our goal is to ensure you receive the maximum coverage you’re entitled to.

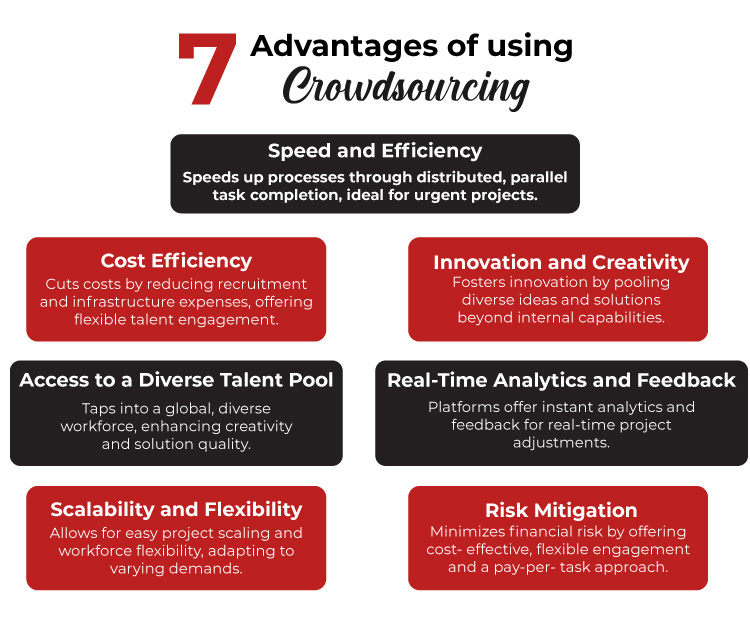

8. Crowdsourcing: Leveraging Community Support

For homeowners facing significant financial challenges, crowdsourcing can be a powerful way to rally community support and raise funds for your roofing project.

This approach is particularly helpful in situations like uninsured damage due to natural disasters, financial hardship preventing necessary repairs, or even for community-driven projects to restore a historic building. It emphasizes the potential for generosity within a community and can significantly alleviate a financial burden.

How Contractors Can Help:

- Discounted Quotes: You may want to consider letting the prospect know you are happy to support their campaign by providing a discounted quote for the roofing project to incentivize donations.

- Donate Services/Materials: You can also offer to donate a portion of your services or materials to the campaign to show your commitment.

- Social Media Sharing: Furthermore, you can share their campaign on our company’s social media channels to increase its visibility and reach a wider audience.

This approach can truly turn a daunting expense into a community effort.

9. Family and Friends: Navigating a Sensitive Topic

Approaching the topic of borrowing money from family and friends can be sensitive, and we understand that. We offer this as just one of several financing possibilities, and there’s absolutely no pressure to pursue it.

- Reframing the Perspective: It can be helpful to reframe the perspective on this type of loan. A new roof is a long-term investment in your home’s safety, structural integrity, and resale value. Your family or friends might see this as an opportunity to help you protect a valuable asset.

- Contractor Support: We’re here to support you in this process. We can provide a detailed, professional estimate that you can share with potential lenders, and we’re happy to answer any technical questions your family or friends might have about the roofing project. For some homeowners, discussing home repairs with family or friends can be a viable way to secure funding. We can provide you with a comprehensive estimate that outlines the project details and costs, which you can share with them. Take advantage of our printing services.

10. 401(k) or Investment Portfolio: Tread Carefully and Advise Consultation

Accessing your retirement funds or investments can be a way to finance a new roof, but it comes with significant drawbacks.

- Significant Drawbacks:

- Penalties and Taxes: Early withdrawals from retirement accounts often incur penalties and taxes.

- Missed Growth: And you’ll miss out on potential future growth, which can significantly impact your long-term retirement savings.

- 401(k) Loans vs. Withdrawals: If your 401(k) plan allows loans, borrowing against the account is generally preferable to a withdrawal. The borrowed amount is repaid with interest, and that interest is paid back into your account, benefiting you.

- Advise Professional Consultation: We strongly advise consulting with a qualified financial advisor before making any decisions about your retirement funds or investments. It’s crucial to understand the full financial implications of such a move.

11. Savings: A Direct and Practical Approach

Don’t hesitate to directly ask your client, “Do you have any savings set aside for home repairs?” This simple question can often lead to a straightforward solution.

- Reframing the Expense: It’s helpful to reframe the expense of a new roof. It’s not merely an expense, but a valuable investment in their property. This is also a key message in [Roofing Marketing Ideas].

- Long-Term Benefits: Emphasize the long-term benefits, such as increased home value, improved energy efficiency, and the prevention of even more costly damage in the future.

12. CDFI (Community Development Financial Institutions): Supporting Underserved Communities

Community Development Financial Institutions (CDFIs) are non-profit organizations dedicated to providing affordable financial products and services, especially to individuals and communities who might not have access to traditional financing.

- Favorable Terms: These institutions often offer loans for home repairs and improvements with more favorable terms than conventional lenders.

- Eligibility Varies: Eligibility requirements for CDFI loans can vary, so we encourage homeowners to research the options available in their specific area. We’re also here to help you gather any necessary documentation or connect you with local CDFIs that might be a good fit for your needs.

13. SBA (Small Business Administration) General and Disaster Loans: For Commercial Properties

Small Business Administration (SBA) loan programs are primarily designed for business owners, not residential homeowners.

- SBA 7(a) Loans: If you’re a business owner, SBA 7(a) loans are general-purpose loans that can be used for various business expenses, including roof repair or replacement for your commercial property.

- SBA Disaster Loans: In cases where roof damage resulted from a declared natural disaster (like a tornado, flood, or hurricane), SBA disaster loans may provide low-interest, long-term financing specifically to help businesses recover.

- Contractor Support: We can support your SBA loan application by providing necessary documentation such as project estimates and contractor information. We’re also ready to answer any questions you or the SBA may have about the roofing project specifications.

14. FHA 203(k) Loans: Comprehensive Renovation Financing

FHA 203(k) loans are specifically designed to finance home renovations, including roof replacement, and are insured by the Federal Housing Administration (FHA).

- Versatile Use: These versatile loans can be used in two main ways: you can either purchase a home that needs significant repairs and finance those renovations within the loan, or you can refinance an existing mortgage and include the cost of renovations in the new loan amount.

- Two Types: There are two types of FHA 203(k) loans:

- Limited 203(k): For smaller renovations that don’t involve structural changes.

- Standard 203(k): For more extensive renovations, including structural repairs.

- More Complex Process: It’s important to acknowledge that FHA 203(k) loans involve more paperwork, specific requirements, and a more complex process than traditional loans.

- Contractor Familiarity: Our company is familiar with FHA 203(k) loan requirements. We can provide detailed estimates that comply with FHA guidelines and coordinate with the FHA 203(k) consultant involved in your project, helping to streamline the process for you.

15. Life Insurance Policy Loan: An Option for Policyholders with Cash Value

This financing option is exclusively available to homeowners who possess permanent life insurance policies, such as whole life or universal life, that have accumulated cash value.

- Favorable Terms: Policyholders can borrow against this cash value, often at favorable interest rates determined by the insurance company.

- Flexible Repayment: Repayment schedules for these loans are typically flexible.

- Impact on Death Benefit: While the policyholder isn’t legally obligated to repay the loan, it’s crucial to understand that outstanding loans can reduce the policy’s death benefit.

- Advise Agent Discussion: We strongly advise homeowners to discuss the potential impact of these loans on their life insurance policy with their insurance agent. We can provide the necessary documentation, such as the project estimate and contract, to help you assess your loan options with your agent.

16. PACE (Property Assessed Clean Energy) Programs: Financing Energy-Efficient Roofing

PACE (Property Assessed Clean Energy) programs are available in certain states and offer a unique financing solution for property owners, both residential and commercial. These programs allow you to finance energy-efficient upgrades, such as cool roofs or solar roofing systems.

- Key Benefits: A key benefit of PACE-financed roofing is the long-term energy savings and environmental advantages it provides.

- Repayment through Property Tax: Repayment for PACE programs is handled through an assessment added to your property tax bill.

- Varying Requirements: It’s important to note that eligibility requirements and program specifics vary significantly by state, and even by county or city. Some PACE programs may also have restrictions on the types of roofing materials or contractors eligible for financing.

If you’re interested in upgrading to an energy-saving roofing system, PACE programs in our state can provide attractive financing options. These programs allow you to finance the project and repay the cost through your property taxes, often with long repayment terms.

17. Manufacturer Financing Programs: Unlocking Exclusive Deals

Major roofing material manufacturers often understand the financial challenges homeowners face when needing a new roof. To help, they’ve created their own financing programs. These programs are typically offered through partnerships with specific financial institutions and are designed to make their products more accessible.

For example, leading manufacturers like GAF, Owens Corning, and TAMKO are known for offering such options. GAF provides various loan types, including deferred interest and deferred payment options, with repayment terms that can range from 2 to 15 years.

Similarly, Owens Corning collaborates with independent roofing contractors in their network to provide financing that might include low monthly payments, 0% financing upfront, and deferred payment plans. TAMKO also gives access to special rates and offers through a third-party homeowner financing vendor for contractors certified to install their products.

These manufacturer-backed programs aim to make high-quality roofing solutions more attainable.

They do this by offering competitive interest rates, flexible repayment terms, and sometimes even additional incentives like rebates or extended warranties when you choose to finance through their preferred channels. So, put on your to-do list to call your favorite supplier and ask them what financing programs they offer.

Closing the Deal: Financing as a Sales Tool

What would it do for your reputation if you became known as the contractor who makes roofing affordable?

Introducing financing options proactively early in the sales process, rather than as a last resort, can be highly effective. The key is to offer tailored solutions that are customized to the homeowner’s circumstances, financial situation, and the scope of their project.

By presenting a range of options, you empower homeowners through choice, allowing them to feel in control of their decisions. This proactive approach is part of effective marketing.

- Transparency and Trust: Always prioritize transparency and trust by being upfront about the terms, conditions, and potential risks associated with each financing method.

- Written Proposals: It’s also crucial to include detailed financing information in your written proposals to avoid any misunderstandings down the line. We can help you get [Roofing Graphics] to help you better explain these roofing financing options.

Scenario: The Savvy Roofer

(Scene: Sarah’s living room. Mark has just presented an estimate for a new roof.)

Sarah: “Thanks for the estimate, Mark. I really appreciate it. But honestly, I need to get a few more quotes before I can make a decision.”

Mark: “I completely understand, Sarah. Getting other estimates is smart. To help you make a truly informed decision, though, let’s take a quick look at the financing options available for this project. That way, when you compare other quotes, you’ll be able to compare the total cost of each, including how you’d pay for it.”

(Later, if Sarah expresses hesitation about the roof’s condition)

Sarah: “The roof definitely looks rough, but I’m just not sure if it’s really time for a full replacement yet. Maybe we can get by with repairs?”

Mark: “That’s a fair question, Sarah. What we can do is explore financing options that would cover both repair and replacement. This gives you the flexibility to choose the best long-term solution for your home without feeling immediate financial pressure. We can make sure you’re covered no matter which path you decide is best.”

(Later, if Sarah needs to consult her partner)

Sarah: “This all sounds good, but I really need to talk to my husband before we move forward on anything.”

Mark: “That’s perfectly understandable, Sarah. A new roof is a big decision for both of you. To help with your discussion, why don’t we quickly review these financing scenarios together right now? That way, you’ll both have all the information you need, and you can feel confident in your conversation.”

Urgency and Value

To encourage timely decisions, combine financing offers with a sense of urgency, such as limited-time promotions or impending weather risks. Utilize Email Marketing and Social Media for promotions, and we do well.

Simultaneously, reinforce the value of your services and the long-term benefits of a new roof, highlighting how it’s a worthwhile investment in their home. This message can be reinforced through strong messaging utilizing your SEO, another one of our services.

Legal and Ethical Considerations

When offering financing, always ensure compliance with all relevant federal and state regulations. This includes adhering to the Truth in Lending Act (TILA), the Equal Credit Opportunity Act (ECOA), and the Fair Credit Reporting Act (FCRA).

- Licensing: It’s crucial to verify that both your company and any financing partners you collaborate with possess the necessary licenses to offer financial services.

- Transparency: Maintain complete transparency in all your financing offers; avoid misleading or deceptive language and clearly and upfront disclose all terms, fees, and interest rates.

- Professional Consultation: Finally, always consult with legal and financial professionals to ensure your financing practices are sound, ethical, and fully compliant. Remember, as a contractor, your role is to guide prospects to options, not to act as a financial advisor.

The Path to a Thriving Roofing Business: Empowering Homeowners Through Financing

By mastering the art of roofing financing, you’ll transform cost objections into opportunities, empower homeowners to make informed decisions, and ultimately, build a more successful and sustainable roofing business.

By strategically offering diverse financing solutions, roofing contractors can transform cost objections into opportunities. Empowering homeowners with choices and clear information builds trust and facilitates informed decisions.

From preferred lender partnerships and home equity options to government programs and even creative solutions like crowdsourcing, a comprehensive approach to financing can significantly boost your closing rates and foster a thriving roofing business.

Remember to always prioritize transparency, adhere to legal and ethical guidelines, and continuously reinforce the long-term value and investment a new roof provides.

Our Mission Is To Help You Reach Your Growth Goals

Now that you’ve explored these diverse roofing financing options, consider how effectively they’re presented to your prospects. Our roofing marketing services can help you seamlessly integrate and highlight these solutions on your website, empowering homeowners to say ‘yes’ to their new roof.

Don’t let financing questions stand in the way of your roofing business’s growth!

Partner with Creative Roofing Marketing and leverage our expertise to transform cost objections into closed deals. We specialize in digital marketing for roofing companies and can help you implement strategies that empower homeowners with diverse financing solutions, from preferred lender partnerships to utilizing home equity and even government programs.

With over 16 years of experience in digital marketing and a team of 10 experts, we’re ready to help you attract more roofing leads and achieve your growth goals. Contact Creative Roofing Marketing today at 559-623-5292. Learn how our proven strategies on web design can boost your closing rates and foster a thriving roofing business.

Want a Roofing Project Financing Questionnaire for Homeowners? Click here and download it now!